A common criticism of rent regulation is that such regulation increases rent inequities among tenants. Controls arguably provide "bargain rents" that induce tenants to occupy regulated units as long as possible, causing older, "empty nest" households to "over-consume" large dwellings which are better suited to the needs of younger, child rearing households seeking entry into the regulated sector. Regulations that do allow special rent increases for vacant units, such as New York's stabilization system, not only encourage long term occupancy, but also promote "rent skewing", in which identical apartments become differently priced over time due to variations in their turnover rates. Through this process, long standing regulated tenants pay much less rent than newcomers to the regulated sector, who in effect "subsidize" their counterparts. According to critics, these drawbacks seriously undermine the utility of controls as a means of making housing more affordable.

The presence of "rent skewing" in New York's stabilized housing would seem to contradict the "fairness" policy upon which the system was founded. However, this observation is based on the assumption that skewing is a unique by-product of rent regulations, and is not common to all types of housing markets. Objective assessment of the equity of skewing in New York's stabilized housing requires knowledge of the presence and degree of skewing in the city's non-regulated housing markets. The purpose of this analysis is to determine: a) the existence and extent of "skewing" within the city's stabilized sector as well as in the private market, b) the effects of "skewing" upon stabilized tenants as well as the city, and c) what actions the Rent Guidelines Board should undertake to either minimize or justify "skewing" within the stabilized system.

These questions will be explored first through a review of existing literature on rent skewing in both regulated and unregulated housing markets. Analysis of two hundred and twenty rent stabilized buildings for the presence of skewing within and between buildings will then be conducted. This analysis will be followed by a more detailed examination of the factors which contribute to any skewing which exists within the stabilized system.

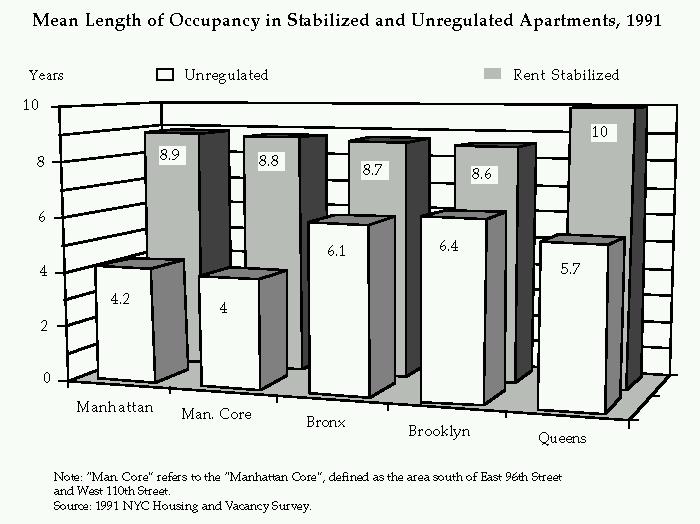

Further examination revealed similar average annual "length of occupancy" discounts (one measure of skewing) for sitting tenants in both sectors, but generally higher average total discounts for tenants in stabilized units than for those in unregulated rentals. This was due to the tendency of tenants to occupy stabilized dwellings for longer periods than other rental units, particularly in Queens and the part of Manhattan lying below 110th Street. Statistical tests undertaken on the length of tenure in stabilized and other rental units revealed a significant (non-random) positive association between stabilized status and length of occupancy.

Anthony Downs was among the first authors to provide a theoretical explanation for rent skewing in the private market. According to Downs, ownership of America's rental stock is dispersed among thousands of small property owners, with more than 60% of all rental units situated in buildings with less than five dwellings. Small landlords, due to the limited size of their holdings, tend to be much more sensitive to the costs incurred from vacancies than to the rents they receive from their property. In effect, Downs believes that small building owners are usually "turnover minimizers", who prefer to keep their units continually occupied, instead of "rent maximizers", who are willing to constantly refurbish vacant units to attract the highest paying tenants.(2) Given these attitudes, small landlords are willing to offer discounts to "good" (i.e., responsible, well behaved) tenants on a continual basis rather than to risk the expense of vacancies.

A number of empirical studies corroborate the existence of rent skewing in the unregulated housing sector. One of the most important is an article written by Allen Goodman and Masahiro Kawai in 1985 for the journal "Land Economics". The authors found statistically significant levels of rent skewing in eighteen out of nineteen metropolitan housing markets across the United States. In this analysis, length-of-tenure discounts averaged 1.3% per year for units of similar quality and location (i.e., the rents of established tenants declined by an average of 1.3% per year of occupancy compared to those of new tenants in comparable dwellings). The value of these discounts averaged eight dollars per month, which equaled 3.7% of the rents charged to new tenants.(3)

Among other authors concerned with private market rent skewing, Ira Lowry mentions a study undertaken by the Rand Corporation of rental properties in Brown County, Wisconsin and St. Joseph's County, Indiana in 1976, which found that monthly gross rents decreased from estimated "market levels" by a mean value of 3.8% per year of occupancy.(4) Another analysis conducted by Arthur D. Little in 1987 examined rent levels in cities with and without rent control and concluded that rents in all cities "...decrease with each year of additional occupancy".(5)

Many studies of rent regulated housing markets allude to rent skewing without exploring the issue in detail. Most link controls with reductions in tenant mobility, by claiming that below market rents encourage sitting tenants to occupy controlled apartments for extended periods of time, dramatically reducing turnover for some units. Systems with special vacancy allowances promote skewing over a period of years between dwellings that turnover frequently and those that do not. Anthony Downs elaborates on this point by observing that controls, in reducing the mobility of the initial occupants of controlled units, create shortages which make it harder to move from one controlled unit to another.(6)

Analyses that empirically examine tenant mobility in rent regulated cities present mixed results on this issue. One study of Los Angeles' rent stabilization system, conducted in 1984, found that tenant mobility in both the city and its surrounding communities (which did not regulate rents at the time) substantially decreased between 1977 and 1984. On the other hand, the authors found that length-of-tenure discounts substantially increased in Los Angeles over the same period, (the city's rent stabilization system was enacted in 1979). Although discounts for tenants with less than two years of occupancy declined between 1977 and 1984, discounts for those with three to four years increased by 39% and those for renters with more than six years of residency nearly doubled. From these findings the authors concluded that, overall, long standing tenants reaped the greatest rewards from stabilization in Los Angeles, whereas recent movers and tenants with less than three years of residence received the least benefits.(7)

Another examination of rent regulation, written in 1976 by Franklin James and Monica Lett, analyzed New York's rent stabilized housing stock. Despite its lack of quantitative sophistication, James and Letts' analysis concluded that the average variation between the highest rents and the lowest rents charged for four different types of apartments was 20% higher in rent stabilized buildings than in rent controlled buildings. The authors attribute this disparity mainly to the use of variable length leases, as well as vacancy allowances for unoccupied units, which they argue will cause skewing to increase over time, particularly during periods of rampant inflation.

To ameliorate this situation, James and Lett propose the exclusive use of one year leases, which, in their view, would prevent skewing from worsening over time.(8) However, James and Lett ignore the crucial option of modifying or eliminating vacancy allowances as a means of either remedying existing skewing or dampening future rent disparities.

Joel Brenner and Herbert Franklin's analysis of European rent controls also examines rent skewing, and provides a useful summary of strategies used to counteract it. Brenner and Franklin's discussion of skewing goes into greatest depth concerning Holland, where rapid inflation during the 1970's created great disparity in rents between new construction and older housing. They focus on two particular anti-skewing policies: a system of subsidies similar to HUD's Section 8 vouchers and a more recent attempt at "rent adaptation", whereby rents in older apartments are raised to levels comparable to new ones. According to the authors, the Dutch abandoned the former in the late 1970's, after rising inflation quickly devalued the subsidies paid out, opting instead to concentrate on "rent adaptation". This refers to a gradual re-alignment of rents in both old and new units, achieved through a series of slight rent increases in older dwellings combined with a new mortgage instrument, in which interest is spread evenly throughout the life of the loan to produce smaller monthly payments.(9)

The simplicity of the DHCR data set precluded detailed insight into the factors behind skewing of rent stabilized rents beyond the fact that variance in rents between similar units (i.e., units within the same line) was positively correlated with location in Manhattan and negatively correlated with building size. Thus, Manhattan addresses were linked to increased differences in rents within apartment lines while larger buildings tended to have greater observed variation within apartment lines.

For non-Netscape table, click here or see end of current page.

| Rent Stabilized Buildings | Unregulated Rental Buildings | |||||

| Location: | Annual Discount | Total Discount | Annual Discount | Total Discount | ||

| Manhattan | 2.6% | 23.4% | 2.6% | 10.7% | ||

| Manhattan Core | 2.8% | 24.6% | 2.2% | 8.9% | ||

| Bronx | 1.3% | 11.4% | 2.0% | 12.1% | ||

| Brooklyn | 1.7% | 14.8% | 2.2% | 14.2% | ||

| Queens | 1.6% | 16.2% | 2.0% | 11.0% | ||

Note: The number of stabilized properties in Staten Island was too low to be statistically reliable.

Source: NYC 1991 HVS

The figures illuminate an interesting relationship between rent skewing and regulation status. It appears that the main factor behind the total level of skewing experienced by tenants in both markets is the length of tenure rather than the annual discounts offered to renters. This is starkly demonstrated in Manhattan and Queens, where mean annual discounts were roughly equal across the sectors, while mean total discounts were much higher in the stabilized market due to mean lengths of occupancy double those in the unregulated rental market. In both the Bronx and Brooklyn, mean annual discounts are higher in unregulated units while the mean total discounts are approximately similar due to longer tenure patterns among stabilized tenants.

See chart Mean Length of Occupancy in Stabilized and Unregulated Apartments, 1991

These findings prompted further analysis of HVS data, to determine whether rent stabilization status significantly influenced length of occupancy, and thus the total amount of skewing observed in the 1991 HVS sample. Additional regression analysis revealed a strong positive correlation between length of occupancy and rent stabilization status among households of similar income in units of similar location, size and quality. Thus, tenants in rent stabilized units have strong incentives to occupy their units longer than their counterparts in unregulated rental dwellings, particularly in Manhattan, and especially in the high rent "Manhattan Core". In turn, this significantly influences the total amount of skewing observed in the stabilized sector.

Length of Occupancy Discounts" in Rent Stabilized and

Unregulated Rental Buildings, 1991

Rent Stabilized Unregulated Rental

Buildings Buildings

-------------------- ---------------------

Annual Total Annual Total

Location: Discount Discount Discount Discount

Manhattan 2.6% 23.4% 2.6% 10.7%

Manhattan Core 2.8% 24.6% 2.2% 8.9%

Bronx 1.3% 11.4% 2.0% 12.1%

Brooklyn 1.7% 14.8% 2.2% 14.2%

Queens 1.6% 16.2% 2.0% 11.0%

Note: The number of stabilized properties in Staten Island was too low to be statistically reliable.

Source: NYC 1991 HVS

To return, click here

{kind=link}